Why Fighting Inflation Is Not a Priority for the Fed

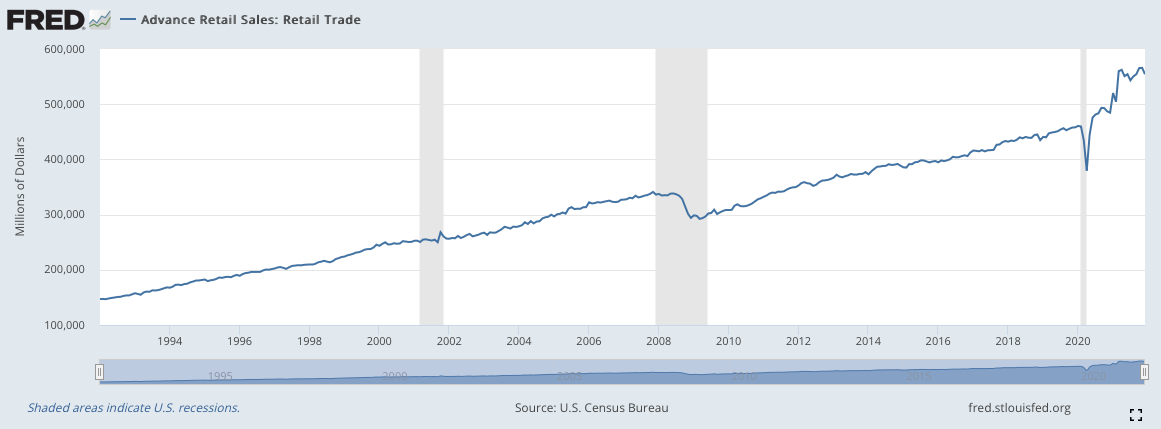

On Wednesday, the Federal Open Market Committee (FOMC) held true to its monetary-tightening timeline despite last week’s 10 percent drawdown in most major indices, effectively saying, “10 percent is not enough.” With retail sales numbers that will surely return to trend without more stimulus (see chart), a gridlocked Senate, and the prospect of higher interest rates surely to discount equity valuations, why aren’t more people selling?

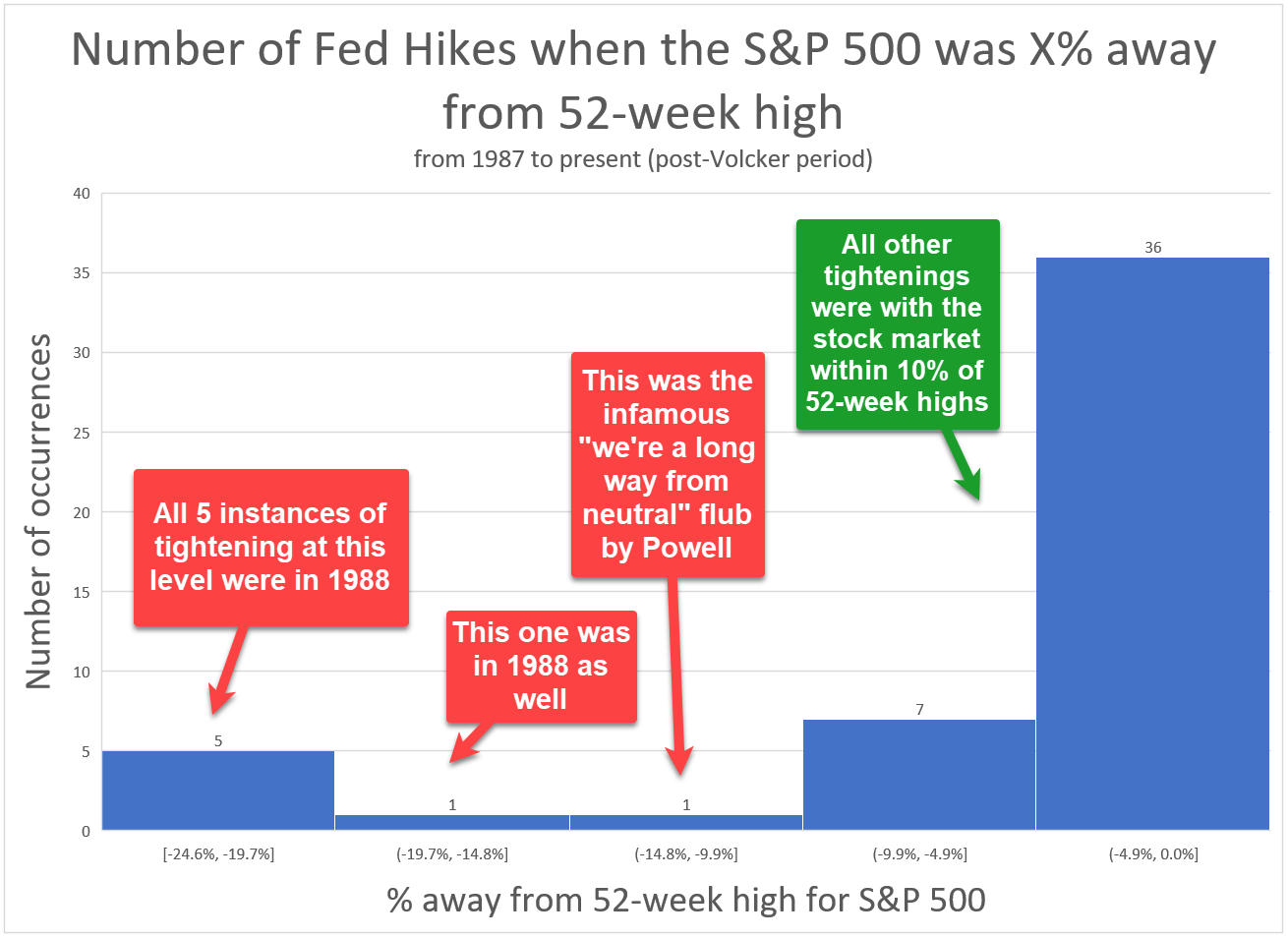

Don’t get me wrong, the Fed will cave eventually, but they just sent a clear message that they need to see more selling. Will they ever make it to “lift off”? This handy chart, courtesy of the Macro Tourist newsletter, can shed some light:

As you can see, there has been just one rate hike post-1988 during which the S&P 500 was more than 10 percent off its fifty-two-week high. This rate hike was enacted by Jerome Powell and set off the infamous Taper Tantrum episode. So, we have two months before he is faced with this decision again. Suppose the market remains relatively flat or even increases between now and March. Given yesterday’s tolerance and historical precedence, I’d bet on lift off proceeding, which would hurt valuations. Alternatively, if the market continues to decline before the March meeting, historical precedence and Powell’s taper trauma tell us there will likely not be a rate hike in March, which is where things will get interesting. Long story short, markets are going down before they go up. I ask again, Why isn’t everyone selling?

Now, when the FOMC finally capitulates, resumption of quantitative easing will be perceived as an admission that looser monetary policy is here to stay and the Fed will do anything to prop up asset prices (if that wasn’t already obvious). This will be the time to buy back in, so why hold on now? The stimulus is not returning until enough people sell, so might as well beat the crowd.

Upon reversal of policy, inflation assets will rally stronger than the broader market (as was the case during QE’s debut in 2008), and to see why this may be a secular inflationary shift, take a look at Biden‘s nominees for the Federal Reserve Board of Governors: Lisa Cook, Sarah Bloom Raskin, and Phillip Jefferson (who’s always mentioned last for some reason).

In regards to mandatory diversity requirements for corporate boards, Cook stated, “I would adopt that rule more broadly.”

Suggested the great financial crisis could’ve been averted if economists had had more diverse “lived experience.” (Source)Believes in wielding policy to “address racial wealth gap.”

Raskin said, “While none of [the US financial regulators were] specifically designed to mitigate the risks of climate-related events, each has a mandate broad enough to encompass these risks within the scope of the instruments already given to it by Congress. Accordingly, all U.S. regulators can—and should—be looking at their existing powers and considering how they might be brought to bear on efforts to mitigate climate risk.”

“[This will require] our financial regulatory bodies to do all they can—which turns out to be a lot—to bring about the adoption of practices and policies that will allocate capital and align portfolios toward sustainable investments that do not depend on carbon and fossil fuels” (Source).“Community reinvestment process to bolster the resilience of low-income communities to climate change” (Source).

Jefferson claimed “CPI is upwardly biased.” In other words, it overreports inflation.

“These findings feed into the current deliberations within the Federal Reserve System in favor of those who would not slow the economy too soon.” Jefferson discusses this in his 2006 paper, arguing that the advantages of overly hot monetary policy outweigh the risks of inflation for low-income families.

While a few quotes do not define a person, they’re worth paying attention to. I get the impression that these people want to expand the Federal Reserve’s power and believe the threat of inflation pales in comparison to climate change and racial inequities. So, in a world where investing largely revolves around guessing how a group of seven people will choose to arbitrarily tinker with our country’s financial system, I’m betting these folks will stay looser for longer.

{kind=link}

{kind=link}