China Needs More Economic Freedom—Not a Bigger Welfare State

China has not been spared heavy criticism about its growth mode since it joined the World Trade Organization (WTO) in 2001. Leading the choir of discontent, the International Monetary Fund (IMF) claimed that “high savings are at the heart of China’s external and internal imbalances.” Other mainstream pundits also believe that China’s mercantilist policy was the main contributor to a global savings glut that depressed international interest rates and inflated asset bubbles all over the world, including in the US. This convenient shift of blame for the root cause of the Great Recession is actually misleading. China has indeed piled up large current account surpluses and international forex (foreign exchange) reserves, but they were not financed with a transfer of real savings from the rest of the world. It was the lax monetary policy of the Fed and other major central banks that financed the purchase of Chinese goods, drove down interest rates to record-low levels, and fueled an unsustainable boom, triggering the Great Recession.

In the aftermath of the Great Recession, China implemented massive domestic growth stimuli, which dented its external competitiveness. As current account surpluses almost dried out, criticism moved toward China’s so-called domestic imbalances. China’s high savings and limited consumption relative to other economies were held responsible for overinvestment in national technological champions and loss-making heavy industries, contributing to international trade frictions. Mainstream economists are recommending that China fix this alleged problem by increasing public spending and making taxation more progressive, and going for a bigger government in general. The IMF argues too that a “reliable and effective social safety system” and a “reduction of the high household savings rate” would rebalance and make “resilient” China’s growth model. But why would high saving and low consumption impede sustainable growth? Both sound economic theory and historic experience refute the mainstream’s claim that China needs a big welfare state like those of modern Western economies in order to get richer.

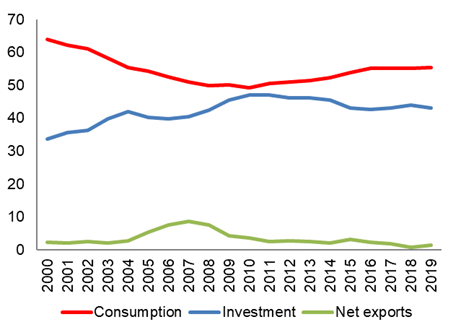

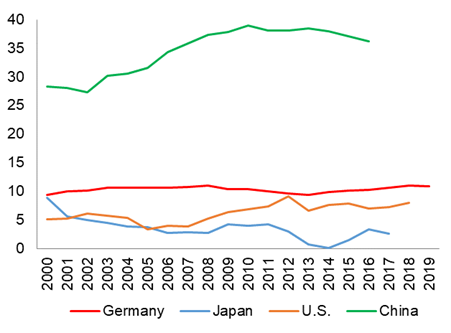

By international standards, China’s household consumption appears low at about 39 percent of GDP in 2019, relative to 60 percent on average in OECD (Organisation for Economic Co-operation and Development) countries and close to 68 percent in the US. Despite an increase since the Great Recession, total consumption, at around 55 percent of GDP, also looks depressed (graph 1). In contrast, China’s investment ratio has traditionally been very high. It had moderated to around 43 percent of GDP by 2019, but is almost double rates recorded in the US, Germany, and Japan, which are slightly above 20 percent. Robust investment is supported by a very high domestic savings rate of about 45 percent of GDP stemming primarily from an extraordinary saving propensity among households. Since the Great Recession, the latter have saved more than 35 percent of their disposable income every year, compared to less than 10 percent by their counterparts in the US, Germany, and Japan (graph 2).

Graph 1: Consumption, Investment and Net Exports in China (Percent of GDP)

Graph 2: Households Savings (Percent of Disposable Income)

The high saving propensity of Chinese households seems puzzling when average disposable income per capita is about 15 percent lower than in the US. Even the poorest households in China display a high savings rate of about 20 percent of disposable income, whereas the savings rates for the bottom 10–20th percentiles are often negative in many countries due to the substantial social transfers supporting their consumption (IMF 2018). According to the IMF, the main contributors to the high saving propensity of Chinese households are the effects of the one-child policy, the transformation of social safety nets during the transition to a market economy, and the surge in private housing ownership. One should add that private consumption has also been artificially depressed by a relatively high taxation of foreign consumer goods and financial repression through the capping of bank deposit rates. Yet before the trade war with the US, China had several rounds of import tax cuts on consumer goods, and bank deposit rates have been gradually liberalized in recent years while household saving rates have remained very high.

After a closer look at China’s social safety nets, it becomes fairly clear that the relatively low taxation and lean welfare system are the key factors behind China’s high saving ratio. After large disruptions in the early 1990s, China has gradually rebuilt universal coverage for old-age pensions and a new healthcare scheme for both urban and rural areas, financed by a mix of social contributions and government subsidies. But China’s social safety nets are much less generous than in advanced economies, in particular in terms of unemployment benefits and pension income for the elderly who have not contributed to the social security system (IMF 2018). In addition, rural households and migrant workers have poorer access to pension benefits and health services compared to the urban population, and out-of-pocket expenditure as a percentage of total health expenditure is also relatively high.

China has focused on reducing extreme poverty through high growth rates that have lifted all incomes but has also implemented social policies such as the “Dibao” system of minimum income guarantee, profarmer policies, hikes in minimum wages, and reductions in the personal income tax. As a result, extreme poverty has been almost eradicated from a rate as high as 66 percent in 1990. At the same time, China has favored a lean welfare system and kept in check total government social spending, which remains low at about 8 percent of GDP, compared to 20 percent in the US and 25 percent in Germany. It’s interesting to note that at the beginning of the 1960s, social spending was also only 7 percent of GDP in the US and 15 percent in Germany (OECD data), while their respective economic growth rates were much higher.

The fact that China has not built a highly redistributive welfare system like in most advanced economies is illustrated primarily by the very limited role played by the personal income tax (PIT) in income redistribution. Due to a high personal allowance threshold, employees of private firms start paying PIT only when their income exceeds 250 percent of the national average wage, and even at this level, they pay less than 1 percent of their income. Only people in the top income quintile are effectively paying an income tax, and one needs to earn 23.5 times the national average wage in private firms in order to pay the highest marginal rate of 45 percent (OECD 2019). As a result, the Chinese budget collects only 1.2 percent of GDP from PIT, compared to more than 10 percent of GDP in the US. Minimum wages, which are set at local level, also have more limited redistributive effects than in advanced economies. At about 25 percent of the average wage, Shanghai has one of the highest minimum wages in China, but this is about the same as the average US minimum wage and about half those of France and Germany. Overall, the tax system is less progressive than in many other countries, with a much higher share of revenues collected by indirect taxation such as VAT (value-added taxes) and other taxes on goods and services.

All this prompts the IMF and other mainstream pundits to call China’s taxation system “regressive” and to call for more progressive income taxation and redistribution. They are particularly critical that a minimum social security contribution payment is required from all employees, which is, furthermore, capped for higher incomes. In addition, migrant workers are not entitled to some public services in urban areas for which they have not contributed financially (the so-called Hukou system). But it seems only fair and less distortive that all beneficiaries pay a price approximating the cost of public services. In reality, China’s lighter taxation system reduces less people’s incentives to work and save compared to other economies.1 At the same time, less welfare redistribution ensures higher workforce participation and less waste relative to the oversized and increasingly unsustainable social safety nets in modern advanced economies. The heavily criticized higher inequality of Chinese society2 actually allows for higher savings, investment, and capital accumulation, reflected in the rapid increase in general living standards over the last three to four decades.

There is also the pertinent question of whether Chinese savings have been allocated in an efficient way, according to market price signals. Here criticism seems justified, as China’s savings have been increasingly directed into large government investment projects and generally less productive state-owned enterprises (SOEs). Unusually large government investment, to the tune of 16 percent of GDP annually—4 percent on budget and 12 percent off budget—has been directed into questionable infrastructure and real estate projects, in particular since the Great Recession. The misallocation of savings has taken place also through the preferential financing of notoriously inefficient SOEs. The latter hold about 40 percent of company assets in China but generate only about 20 percent of profits and are twice more indebted relative to their equity compared to private companies. Their productivity is about 20 percent lower than that of private firms according to the IMF. Moreover, the government is still reluctant to loosen its grip on the economy by streamlining the oversized SOE sector, which has been remarkably stable at around 25 percent of GDP for nearly a quarter of a century. The new growth blueprint, the so-called Dual Circulation Strategy announced recently, still features a prominent role for the public sector and SOEs in spearheading China’s renewed focus on innovation and technological progress.

In conclusion, the mainstream criticism of China’s high savings propensity, lean welfare system, and reduced progressivity of taxation seems utterly misplaced. China needs high savings and investment in order to support capital accumulation, rapid growth, and convergence of standards of living. This is how current advanced economies grew rich as well—by having limited governments and tax burdens until approximately the beginning of the twentieth century. But the West grew rich also by limiting the regulatory burden and upholding individual freedom in terms of economic decisions, consumption, and investment. China still has a long way to go before people can see their savings properly invested in free markets in order to allow for higher consumption levels in the future. China has become a global manufacturing hub and remained a prime destination for FDI (foreign direct investment) even during the trade war with the US, but the current state capitalist system continues undermining its efforts for a rapid income convergence with more advanced economies.

- 1. For a thorough analysis of government-induced distortions via taxation, see Rothbard Murray N. Rothbard, Man, Economy and State with Power and Market, 2d scholar’s ed. (Auburn, AL: Ludwig von Mises Institute, 2009), pp. 1149–252, https://cdn.mises.org/Man, percent20Economy, percent20and percent20State, percent20with percent20Power percent20and percent20Market_2.pdf.

- 2. The GINI coefficient increased from 0.28 in 1983 to 0.47 in 2019, making China one of most unequal countries in the world.