Real Wages Fall Again as Inflation Stays Near 40-Year Highs

Inflation is so high in America that we’re now supposed to believe that inflation is “moderating” if it doesn’t go above 8.5 percent. That, at least, was the message in much of the speculation yesterday around what April’s CPI inflation numbers would show. Much of the “consensus” was that inflation would come in around 8 percent, and that inflation overall had peaked and is therefore moderating. It’s too early to know if inflation has peaked, but one thing if for sure: there’s no reason to celebrate yet another month of wealth-killing inflation at levels not seen in decades. After all, once purchasing power is lost to inflation in our modern economy, it’s gone forever. The central bank will never allow inflation to persist for any sizable period, so that purchasing power will never be returned to dollar holders.

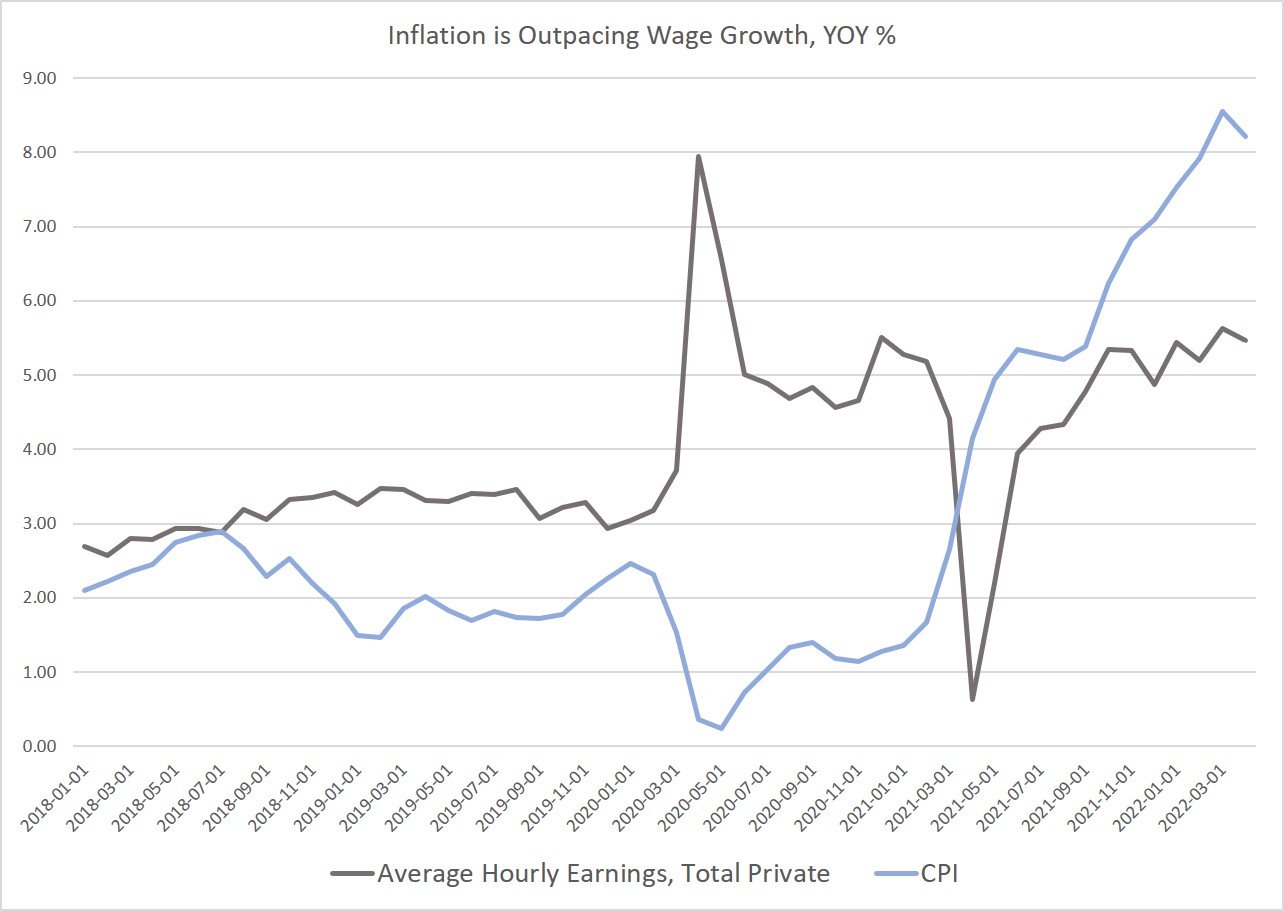

As it is, the BLS’s new official inflation numbers today showed an 8.3 percent year-over-year increase for April. That’s the second highest number in 40 years, but it does show a small decline from March’s YOY inflation increase of 8.6 percent. Much of the price growth was driven by food, energy, vehicles, and transportation. In April, food was up 9.4 percent, year over year, while energy was up 30.3 percent during the same period. Used cars were up 22.7 percent. All items less food and energy were up 6.2 percent.

Yet again, wages were not keeping up. In April, year-over-year growth in average hourly earnings were up 5.4 percent. But that’s down from March’s year-over-year growth of 5.6 percent. This puts the gap between earnings and inflation at -2.8 percent. This is the thirteenth month in a row during which earnings have fallen behind price inflation.

That is, ordinary people have been getting poorer now for more than a year. Grocery bills have continued to mount, and the price of gasoline, while volatile, is hardly on a downward slope. Gas prices have been hitting new highs in May. The national average for gas prices hit $4.37 per gallon on Tuesday.

Looking at the misery index, which combined unemployment and inflation, the total was at 11.8 in April, which puts the index at the fourth-highest level in more than a decade. The White House and regime-supporting pundits have been quick to crow about low unemployment rates, but with wages that can’t keep up with prices, low employment rates are not delivering actual growth in wealth. Some workers may be picking up on this since labor force participation in the 25-54 age range has still not returned to 2019 levels.

The news was grim enough that the White House put out a new statement on inflation this morning:

While it is heartening to see that annual inflation moderated in April, the fact remains that inflation is unacceptably high. As I said yesterday, inflation is a challenge for families across the country and bringing it down is my top economic priority.

This starts with the Federal Reserve, which plays a primary role in fighting inflation in our country. I thank the Senate for confirming Dr. Lisa Cook to the Board of Governors last night, and urge the Senate to confirm my remaining nominees without delay. While I will never interfere with the Fed’s independence, I believe we have built a strong economy and a strong labor market, and I agree with what Chairman Powell said last week that the number one threat to that strength – is inflation. I am confident the Fed will do its job with that in mind.

Beyond the Fed, my inflation plan is focused on lowering the costs that families face and lowering the federal deficit. Already this week, my Administration has announced new steps in partnership with the private sector to lower the price of high speed internet for tens of millions of Americans.

In a similar address yesterday, Biden busied himself with blaming Moscow and covid for inflation. In this new statement, Biden essentially says that inflation is the responsibility of the Federal Reserve, and then moves on to listing the welfare that the administration is planning for constituents.

Importantly, however, Biden invokes imaginary “Fed independence” to explain why he can’t actually do anything directly about inflation. This is a convenient ploy, to say the least. Fed independence has never been a real thing, however, and it’s long been clear that the White House—regardless of political party—habitually pressures the central bank to keep the easy money flowing so as to keep official GDP growth numbers high. This is good politics from the position of elected officials.

Unfortunately for Biden, consumer price inflation has finally caught up with the runaway money creation of the past decade and can no longer be denied. This puts pressure on the Fed and the federal government to “do something” about inflation. This political reality can force the central bank to finally rein in money creation by allowing interest rates to rise and to reduce money-creating asset purchases. This is bad news for the ruling party in that such changes are likely to set off a recession.

Yet, even now, with price inflation at 40-year highs, the Fed is still unwilling to take anything but the smallest most cautious steps toward reining in inflation-inducing monetary growth. The Fed has been talking about addressing inflation since late last summer, yet it’s now May 2022 and the Fed has still not executed a reduction in its balance sheet—which would shrink the money supply and lower asset price inflation—the target federal funds rate remains near historic lows. This isn’t an “independent” Fed doing this. This is a Fed desperate to find a way to reduce inflation without upsetting the political apple cart. There’s little room for error, too, since the economy contracted in the first quarter of this year and signs point toward mounting economic weakness.

But there is one thing the administration could do directly to bring down inflation: reduce deficit spending. This would reduce the political pressure on the Fed to keep interest rates low so as to keep debt service on the federal debt low. Interest rates would then likely creep upward faster and inflation would be (somewhat) mitigated. Meaningful cuts to federal spending, however, aren’t in the cards, especially as both parties ready to massively increase federal military spending.

{kind=link}

{kind=link}

{kind=link}